Robinhood is one of the most popular online brokerage firms today, especially among younger investors who actively trade. During COVID, Robinhood famously restricted trading in 13 stocks on January 28, 2021. As a result, thousands of investors were unable to buy or sell, and billions of dollars in value swung during the freeze.

Robinhood does not charge trading commissions. Instead, it sells order flow to hedge funds and other institutional investors. Its app also gamifies investing, which attracts engagement but can encourage excessive trading. Be careful. Historically, active trading has been a losing strategy compared to disciplined long term buy and hold investing.

Whatever you think about Robinhood’s practices, the company has created significant shareholder value since its mid 2021 listing. The stock went from $35 to $8 and then to over $70. Credit to the Robinhood team for building a highly profitable and resilient business.

As investors, however, we must differentiate between investing in Robinhood the company (HOOD) and investing in Robinhood products. That distinction matters when evaluating the listing of Robinhood Venture Fund I (RVI) and its potential impact on Fundrise’s venture capital listing (VCX), in which I am an investor.

Fundrise is a long-time sponsor of Financial Samurai as our investment philosophies are aligned. All opinions are my own and this article has not been read or vetted by Fundrise before publication. I’ve spent over 15 hours writing and thinking about how I should proceed and what might occur after the listing.

The Robinhood Venture Fund I Offering

Although Robinhood launched its venture fund after Fundrise launched theirs, Robinhood’s larger customer base and platform reach are generating more attention around its planned NYSE listing.

That creates an interesting dynamic. Fundrise investors get to observe how Robinhood Venture Fund I trades before Fundrise’s product lists. In poker terms, Fundrise and its investors have position. We get to see how the market reacts to a similar vehicle, but with different holdings, before deciding whether to buy or sell.

Shares of RVI will be offered through an IPO process on Robinhood’s platform, allowing retail investors to request allocations directly. The anticipated offering price is $25 per share. Like Fundrise’s venture product, participation does not require accredited investor status or large minimum commitments, making it broadly accessible.

The fund will charge an annual management fee of approximately 2 percent, reduced to 1 percent during the first six months after launch. There is no performance fee. The portfolio will adhere to diversification guidelines, with individual holdings capped at 20 percent of assets. Because its Databricks position exceeds that threshold, RVI intends to purchase additional shares of Stripe to rebalance exposure.

Why This Listing Matters For Fundrise Venture

The central question is simple. Will the market assign a premium, par value, or discount to a retail accessible closed end fund that owns high demand private growth companies?

If RVI trades at a meaningful premium to NAV, it signals strong retail appetite for scarce private assets wrapped in a public structure. That would materially increase the probability that Fundrise Venture trades at par or better.

If RVI trades flat or at a discount, then expectations for Fundrise Venture should be recalibrated.

In terms of market conditions, we are in a difficult one right now with the war and elevated volatility. So the timing for RVI’s launch isn’t ideal, maybe a 5 out of 10. So if RVI can manage to trade up, I think that would be a big win.

At any rate, RVI becomes a live market test for how retail investors price illiquid private exposure once it trades daily on the NYSE.

Robinhood Venture I Holdings (RVI)

RVI’s largest holding is Databricks at about 23 percent. Databricks helps companies organize, clean, store, and analyze massive amounts of data so they can build AI applications. It is an infrastructure layer that makes AI possible for enterprises, which is why it should be a core holding for those who believe in AI’s growth.

RVI’s other three major holdings are Revolut at approximately 14 percent, Mercor at about 14 percent, and Airwallex at 7 percent. The combined total of these four holdings is about 59 percent.

RVI is a fintech payments heavy fund, which I’m not sure is the most promising mix. However, given the distribution of Robinhood and the scarcity of such funds, I’m estimating there is a 60% probability RVI trades at a premium to NAV. Before the U.S. bombed Iran, I thought the probability was closer to 75%.

Fundrise Venture Product (VCX)

Fundrise Venture, by contrast, has the two dominant AI pillars in its top four: Anthropic at 20.7 percent and OpenAI at 9.9 percent. The Databricks holding of 17.7 percent roughly cancels out RVI’s holding of Databricks at 23 percent, which is going below 20 percent after RVI purchases Stripe, another payments/fintech company.

Given the entire debacle withe Anthropic, OpenAI, and the Department of War before launching strikes against Iran, the entire AI LLM space has increased its profile. Claude by Anthropic became the #1 downloaded app in the Apple Store for over a week. OpenAI swooped in to land a $200 million DoW contract and likely many more form the government.

Overall, the AI pie will continue to grow, which is one reason real estate in cities like San Francisco should perform well. Besides investing in publicly listed funds that own private AI growth companies, one of the easiest ways to profit from AI’s growth is to buy real estate in cities where these companies are based.

Which Would You Rather Own?

That leads to the strategic question.

Which combination is more likely to command investor attention, long term impact, and sustained profitability: Revolut and Mercor, or OpenAI and Anthropic?

From a market psychology standpoint, OpenAI and Anthropic carry far more brand recognition and narrative power. They sit at the center of the AI transformation. Retail demand often follows familiarity and perceived dominance. Revolut and Mercor are less widely known among United States investors, which may limit enthusiasm.

Revolut provides online multi-currency accounts for individual and business customers, currency exchange and money transfer services, as well as a range of tools to budget, save, and invest. It is also a London-based fintech company, which may dampen U.S. investor demand, as we have seen with Pershing Square Holdings.

By contrast, Mercor is based in San Francisco and connects human expertise with AI development needs. It pays skilled professionals to complete structured tasks such as filling out forms, writing detailed reports, or evaluating AI outputs. Mercor acts as the intermediary: AI labs and tech companies pay for access to tailored, human-generated data, and Mercor compensates the freelance experts.

However, Revolut (~$75 billion valuation) and Mercor (~$10 billion valuation) are far smaller companies than OpenAI (perhaps $860 billion valuation) and Anthropic ($380 billion valuation). Therefore, there could be greater percentage upside in Revolut and Mercor.

However, I worry that OpenAI and Anthropic could easily disintermediate Mercor’s middleman business. As for Revolut, I’m not sure why I need to hold and exchange 28+ fiat currencies or use a Revolut card to make ATM withdrawals or invest in stocks and crypto, as they market.

Personally, as a fund investor and not an angel investor, I would rather own the gorillas – OpenAI and Anthropic – than the smaller upstarts that have a greater chance of going out of business.

Comparing The #4 Holding: Airwallex versus Anduril

I was already feeling pretty good about owning OpenAI and Anthropic through Fundrise after the Department of War debacle. Ultimately, I think Anthropic will work something out with the government given the government needs Anthropic to win the AI global race. Meanwhile, OpenAI is going to continue winning large contracts, although it’s currently going through a PR crisis thanks to its CEO.

However, on March 3, 2026, Anduril, Fundrise Venture’s 4th largest holding, announced it had raised $4 billion and a $60 billion valuation. This is double its $30 billion valuation in June 2025. With the Iran war breaking out, Anduril’s business of building AI-powered autonomous military systems – things like drones, surveillance networks, autonomous submarines, and software that coordinates them – has become front and center.

Meanwhile, Airwallex is another financial technology company that helps businesses move money internationally, manage multiple currencies, and accept payments globally. I guess that’s good. But RVI already has Revolut and soon to own Stripe. Airwallex simply does not have the same impact of Anduril in this current time.

Therefore, if we compare each fund’s #4 holding, I feel like Fundrise Venture easily wins.

How I Invested Pre Listing Of Fundrise’s Venture Product

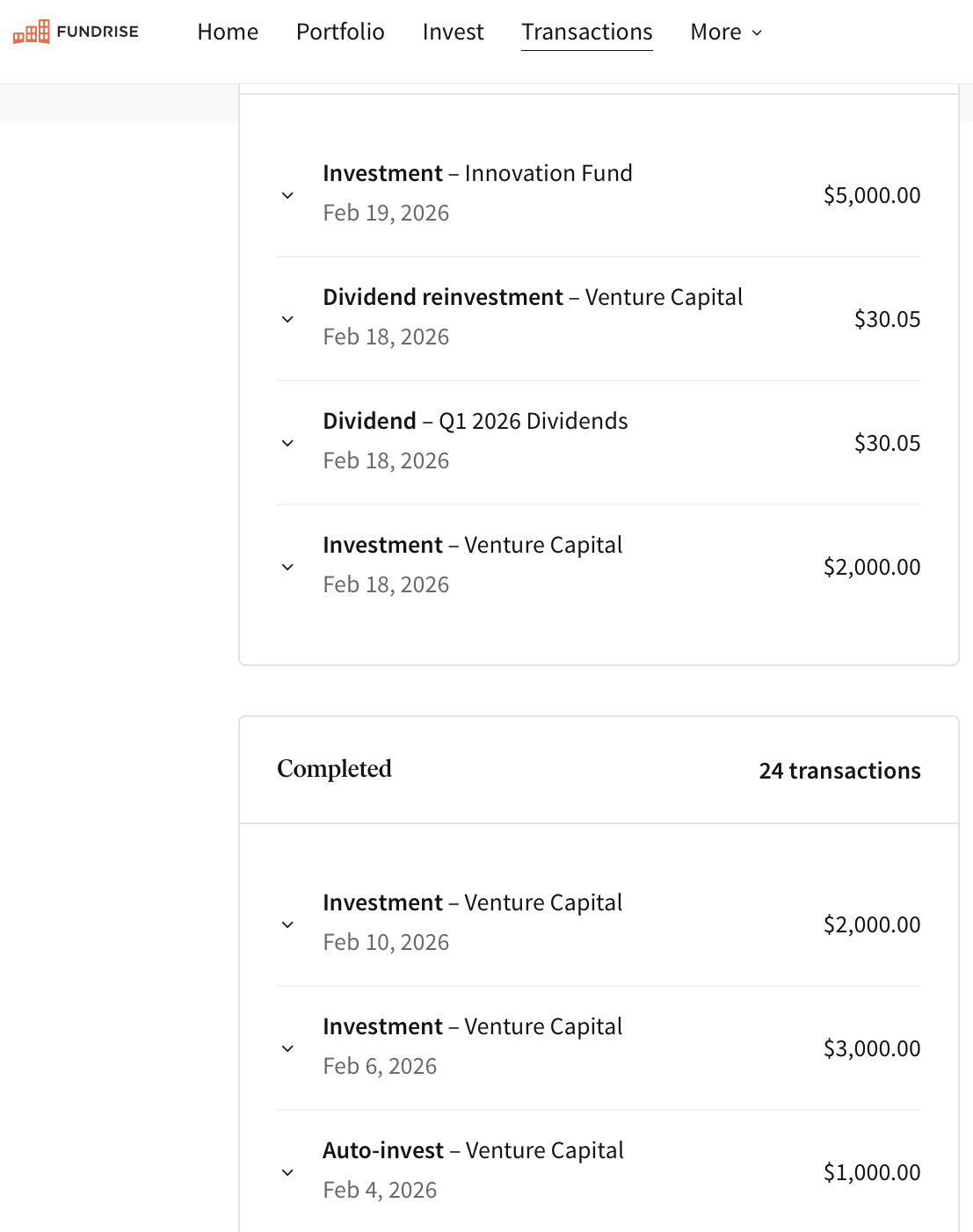

After writing my initial post on what Fundrise’s Venture product listing means for investors, I decided to invest $3,000. Four days later, I invested another $2,000 after taking in more feedback and thinking through the situation further.

After writing another post on why Pershing Square trades at a discount to NAV, and another post on how various fund types trade, I decided to invest another $2,000. The next morning, I invested another $5,000, which turned out to be the final time I could invest because Fundrise closed the ability to invest that night. All told, I invested an additional $12,000.

Funny enough, an email was sent out on March 2, 2026 at 10 a.m. PST saying my window of opportunity to invest up to another $10,000 with no lock-up restriction was open , and I missed it. Why? Because I was relaxing in the hot tub and listening to music. When I finally checked my email at 11:27 a.m. PST, I saw a new message saying my window had already closed. Ah, this luxury expense might end up costing (or saving) me thousands.

If the window to invest was only open for about an hour, I’m assuming demand was strong. Luckily, my wife was able to invest through her own account, which includes the corporate account she manages.

How Fundrise Venture Could Trade Depending On RVI

If RVI trades up and at a premium to NAV, then Fundrise Venture will likely trade at a premium as well. I like Fundrise’s holdings better, but Robinhood is a much larger and more widely known platform.

If RVI trades at par or at a discount of up to 10%, then Fundrise Venture may still trade at a slight premium given its superior holdings.

If RVI trades at a 10%–20% discount to NAV, then I suspect Fundrise Venture will trade flat to down 10%. And if RVI trades down 20%–30%, I’m guessing Fundrise Venture will trade down 10%–15%.

However, in the situation where Fundrise Venture trades down 5% or more, I will likely continue to dollar-cost average with my cash flow, as I did with $2,000 – $5000 investments when the announcement was first made. Being able to buy Anthropic, OpenAI, Databricks, and Anduril at a discount when they are trading at ~40% premium valuations in secondary markets is a win.

Fundamentally, I think the top holdings in Fundrise Venture will continue to grow over the next 5-10 years. As a result, I want to be a long-term investor in these names as the NAV for Fundrise’s venture product continues to grow.

Readers, how do you think RVI will trade? And where do you think RVI will be in a week, a month, and a year from now? How do you think RVI’s performance post listing will affect Fundrise’s venture product?

Author and Investor Background

I first started investing in Fundrise’se venture product in 2023 and currently have over $770,000 invested. Fundrise has been a long time sponsor of Financial Samurai as our investment philosophies are aligned.

My target allocation to alternatives is up to 20 percent of net worth. Approximately 80 percent of my net worth remains in public equities and physical real estate, if we exclude the value of Financial Samurai.

I retired from banking (equities) in 2012 after 13 years. After investing since 1995, I am focused on preserving and compounding capital, not swinging for home runs. That is why I prefer diversified venture funds over concentrated angel bets that mostly go to zero.

Given my risk profile, I would rather pursue a fund that could return 25 percent with a 25 percent drawdown than one that could return 70 percent with a 70 percent drawdown. The more capital you accumulate, the more important capital preservation becomes.

I founded Financial Samurai in 2009, and it has since been read by more than 100 million people. My mission is to help you achieve financial freedom sooner rather than later, based on real world experience and disciplined decision making.

Read the full article here